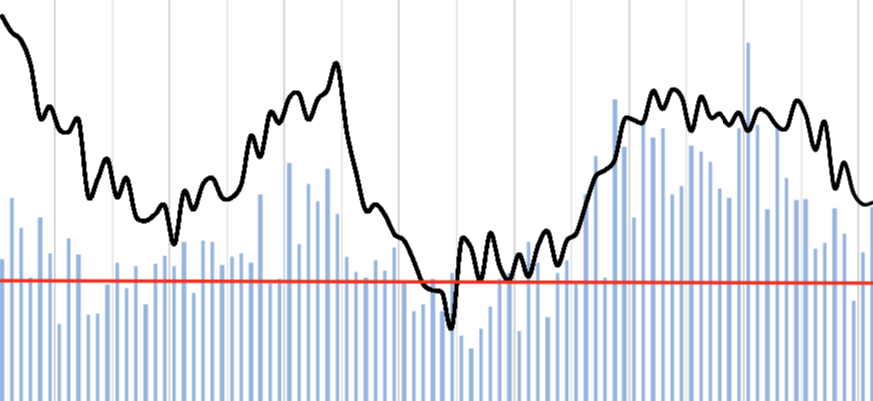

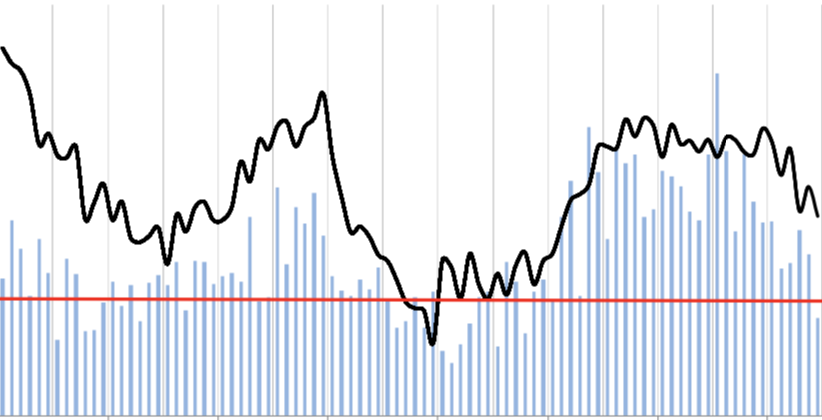

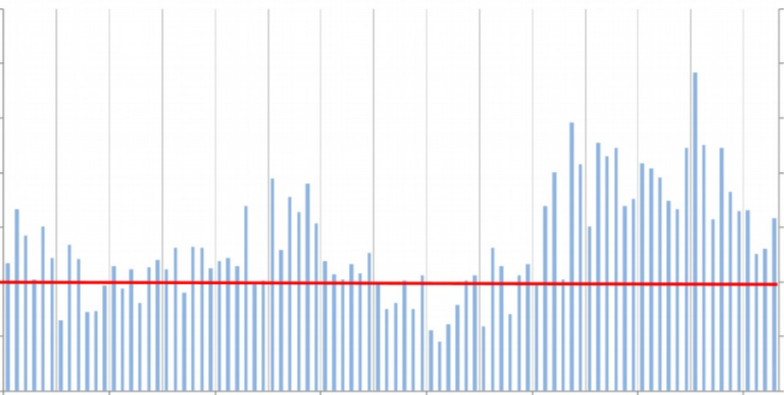

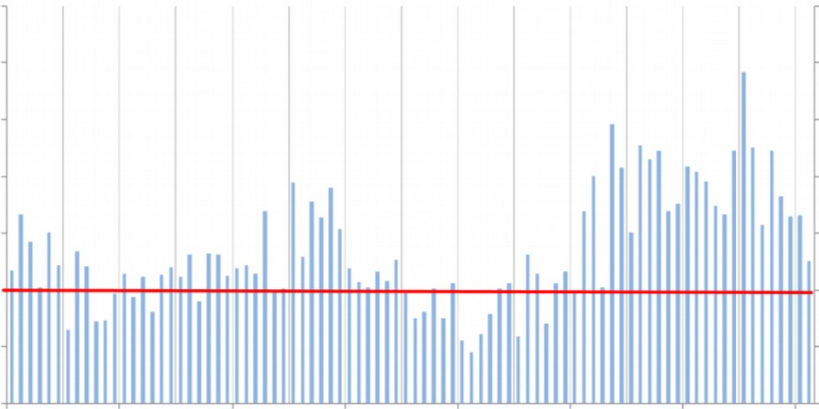

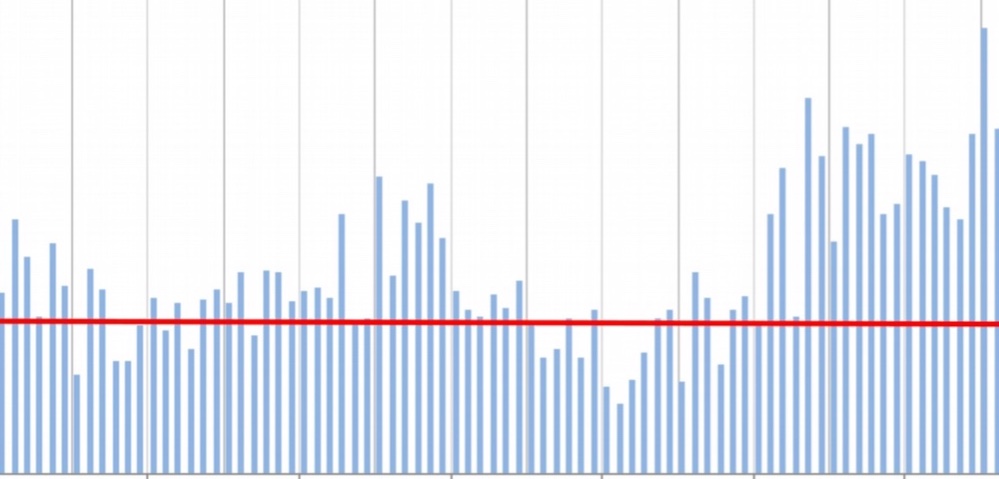

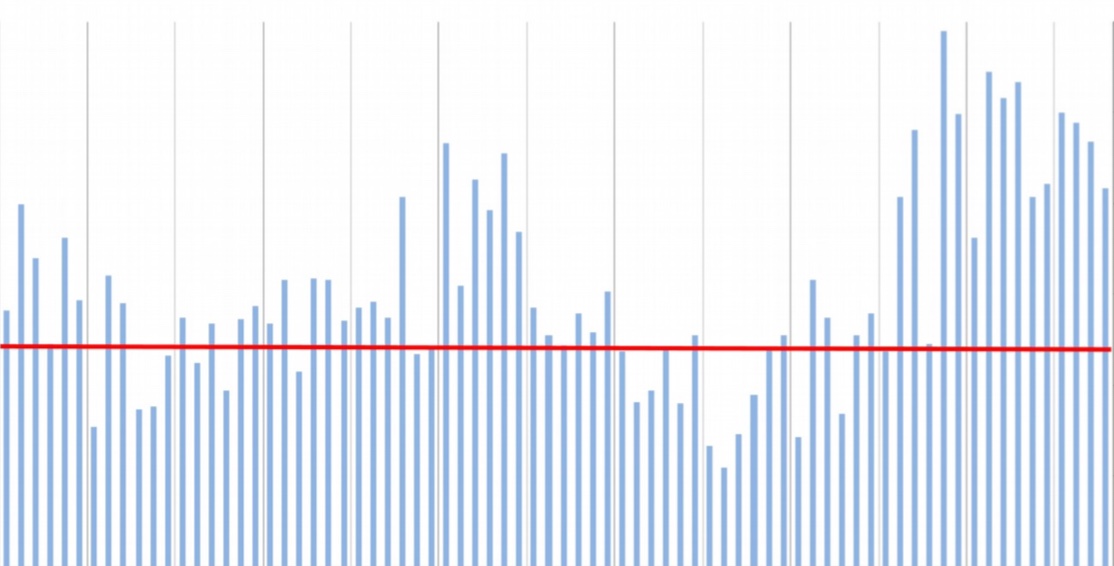

Strong sales, distributor inventories and pricing meet lower employment and customer inventories.

Tag "FDI"

April 06

21:56

2020

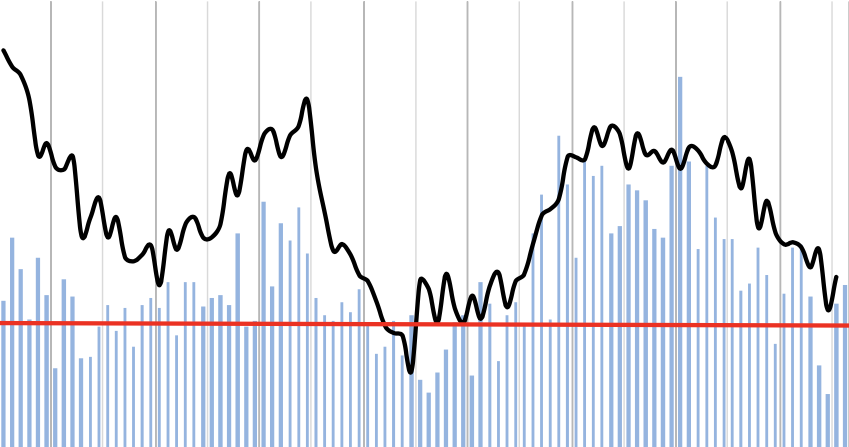

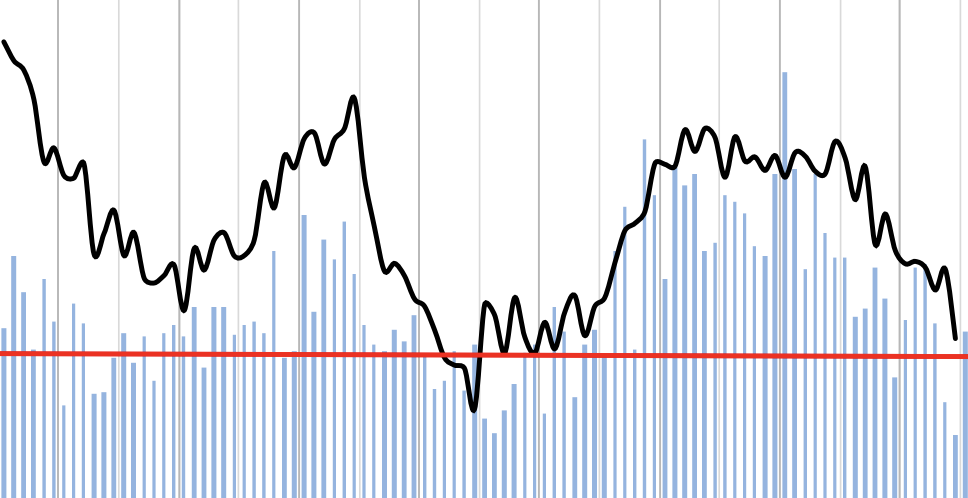

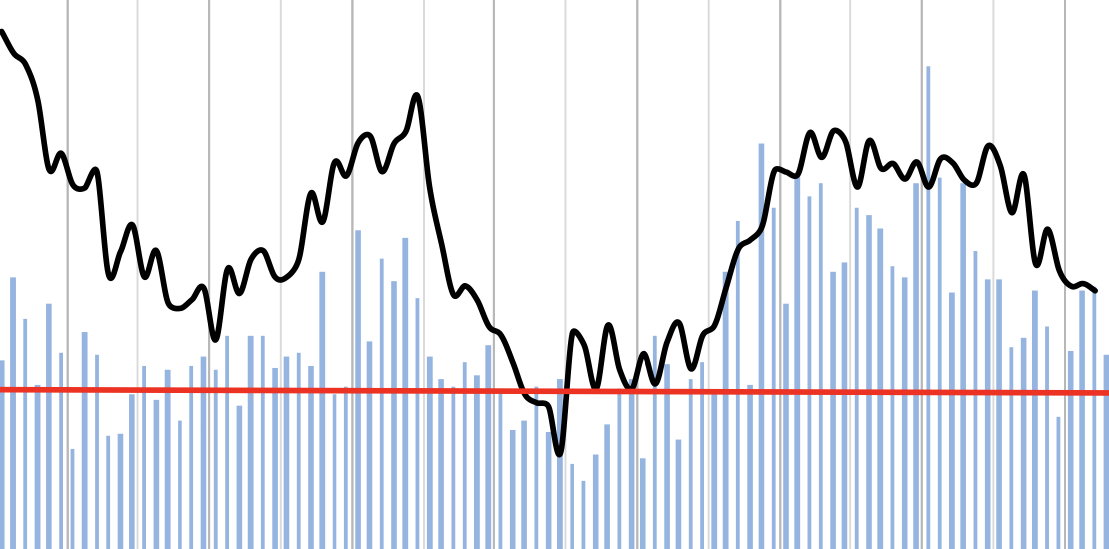

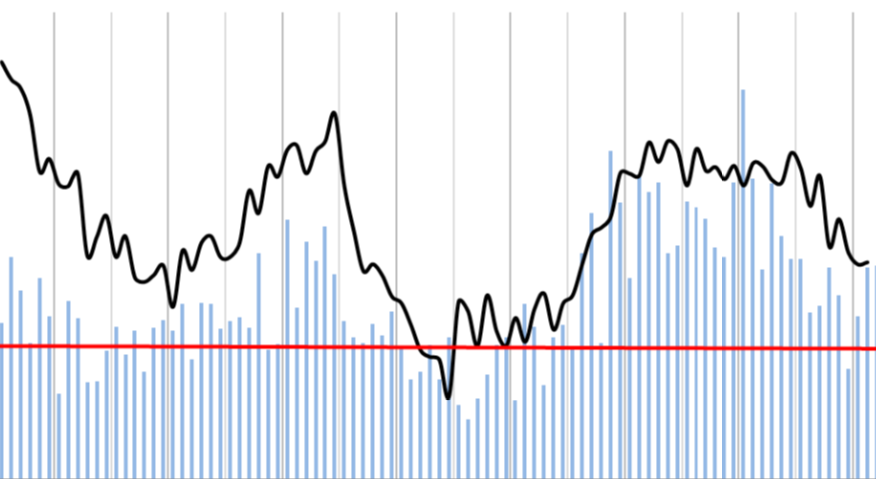

The seasonally adjusted March FDI (44.4) experienced a sharp contraction (February 53) “as the COVID-19 pandemic and ensuing shutdowns took hold over the latter half of the month,” R.W. Baird analyst David Manthey wrote.

March 17

03:20

2020

“Of note, the improvement in the sales index was driven mainly by the seasonal adjustment factor, as the percentage of respondents seeing better-than-expected sales actually decreased vs. last month, although this is not usual given February is normally a seasonally weaker month,” R.W. Baird analyst David Manthey wrote.

February 24

09:44

2020

About 53% of respondents saw sales growth above seasonal expectations, while 23% characterized sales as below seasonal expectations.

January 09

12:22

2020

For the second consecutive month, 56% of respondents saw sales growth below seasonal expectations, while just 19% characterized sales as above seasonal expectations.

November 14

15:02

2019

“Sales trends were slightly improved on an unadjusted basis, but the seasonal-adjustment factor drove the sales index down (month-to-month),” according to R.W. Baird analyst David Manthey.

October 28

04:02

2019

“Better sales trends were offset by a weaker employment reading,” according to R.W. Baird analyst David Manthey.

October 01

02:22

2019

“Better sales trends and a slight improvement in the employment index were the main contributors of the improvement,” according to R.W. Baird analyst David Manthey.

September 03

04:09

2019

“A slight uptick in the percentage of respondents perceiving customer inventory levels as 'too low' was the primary driver of the recovery,” writes R.W. Baird analyst David Manthey.

May 06

16:10

2019

“Sales trends rebounded nicely from weak March trends, which saw a contractionary sales reading,” according to R.W. Baird analyst David Manthey.

March 25

03:17

2019

“Stabilization or further moderation in the FDI could be more likely than acceleration from here,” according to R.W. Baird analyst David Manthey.

February 14

02:39

2019

Several respondents expressed “cautious optimism” for a potential resolution to the US-China trade dispute. Pending any resolution, however, tariffs continue to impact lead times and pricing.

February 04

05:31

2019

Sales trends improved in December, with 42% of respondents indicating sales were “better” relative to seasonal expectations vs. 34% of respondents the previous month.

January 07

04:05

2019

November Fastener Distributor Index decelerates on weaker sales trends.

November 12

02:12

2018

Sales and hiring increased during the month, while customers expressed uncertainty about future orders due to U.S. tariffs.

October 22

03:42

2018

The seasonally adjusted September FDI (55.8) decelerated in September, “still strong in absolute terms but nonetheless meaningfully lower for the second straight month,” according to R.W. Baird analyst David Manthey.

September 24

18:05

2018

“The overall tone of qualitative commentary was again more cautious this month, with respondents expressing some tariff-related uncertainty, and the potential for a loss of momentum,” writes R.W. Baird analyst David Manthey.

July 16

22:00

2018

After four straight months of decline, the FDI regains its footing amid pricing gains and a stronger outlook for the coming months.

May 29

00:43

2018

Qualitative commentary on market conditions was very positive regarding demand, while steel tariff impacts remain a topic of heavy discussion among respondents.

April 10

13:00

2018

Commentary on market conditions was mixed, with some respondents commenting on the current strong demand environment and others expressing concerns around the recently announced steel tariffs.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}